The Debt Service Coverage Ratio (DSCR) loan, a real estate financing tool, requires strong financial history, minimum 1.2 DSCR, substantial property value, and reliable utility easements. Lenders carefully analyze easements, financial statements, and appraisals, considering their impact on property cash flow and borrower repay ability. Transparent and meticulous record-keeping, including easement details, enhances loan approval chances. Lenders assess each application uniquely, prioritizing easement clarity for a successful underwriting process.

In today’s dynamic financial landscape, understanding the intricacies of DSCR (Debt Service Coverage Ratio) loan requirements is paramount for both lenders and borrowers. Easement on these criteria can unlock access to capital for viable projects, fostering economic growth. However, navigating the stringent conditions can be a challenge. This article delves into the core components of DSCR loans, elucidating the criteria that define eligibility. By providing a comprehensive guide, we empower readers with the knowledge to successfully navigate this process, ensuring both parties benefit from a mutually advantageous arrangement.

- Understanding DSCR Loan Basics: Eligibility Criteria

- Financial Analysis for DSCR: Calculating Easement

- Documenting Income & Expenses: A Clear Pathway

- Lender Considerations & Approval Process

Understanding DSCR Loan Basics: Eligibility Criteria

Understanding DSCR Loan Basics: Eligibility Criteria

In the realm of real estate financing, the Debt Service Coverage Ratio (DSCR) loan stands as a robust instrument for both developers and investors. A DSCR loan’s primary allure lies in its ability to facilitate development projects by easing financial constraints, especially when securing funding for utility easements. These loans are designed to ensure a project’s viability by measuring the borrower’s ability to cover debt service obligations against their expected operating income.

Eligibility for a DSCR loan hinges on several key factors. Firstly, borrowers must demonstrate a solid track record of financial performance, often through comprehensive financial statements. This includes proof of income, expenses, and existing debt obligations. For real estate projects, West USA Realty experts advise that a minimum DSCR of 1.2 is typically sought, indicating that the property’s cash flow can comfortably cover debt payments. Secondly, the property itself must possess substantial value and a stable future cash flow potential, making it an attractive investment for lenders.

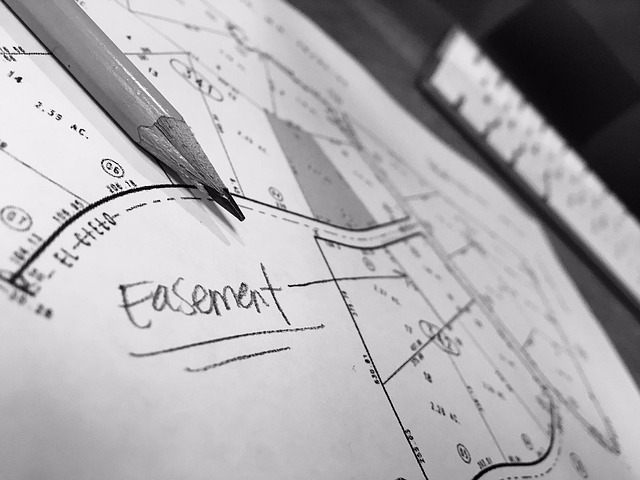

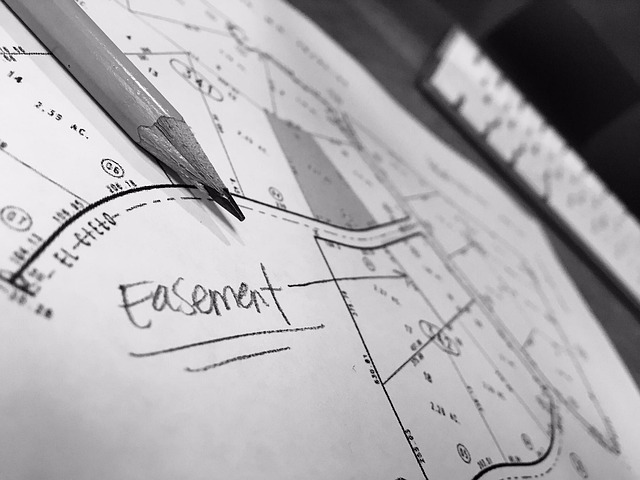

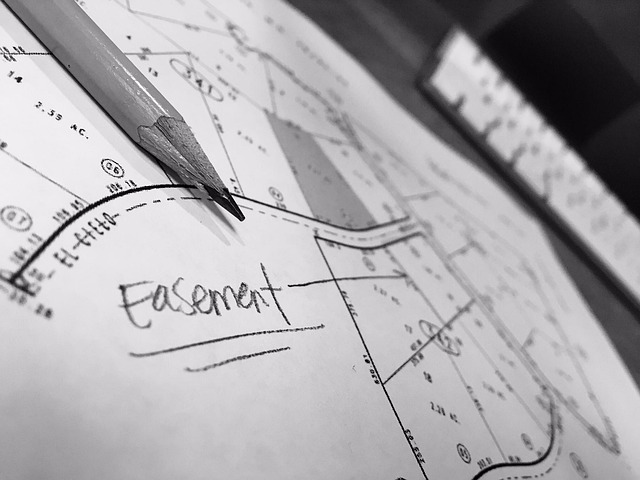

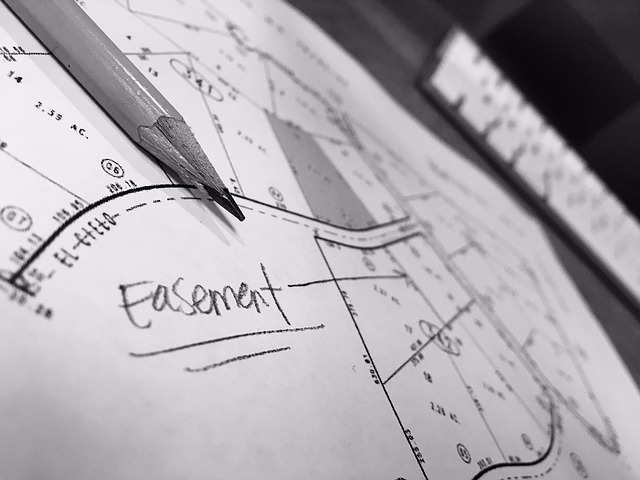

A crucial aspect of DSCR loan eligibility involves the role of utility easements. These easements, whether for power, water, or other essential services, are vital to project feasibility. Lenders assess the utility infrastructure’s reliability and the easement’s long-term stability as a sign of the project’s overall viability. In some cases, securing a utility easement before applying for a DSCR loan can expedite the process, as it demonstrates a clear path to project completion. For instance, a residential development with a guaranteed water supply easement may find it easier to secure financing, as the utility is a reliable and essential component of any thriving community.

Financial Analysis for DSCR: Calculating Easement

Financial analysis is a critical component of any loan application, especially for DSCR (Debt Service Coverage Ratio) loans. When evaluating a property for a DSCR loan, one key aspect to consider is the easement and its potential impact on the financial health and utility of the asset. An easement, in simple terms, is a legal right to use another person’s property for a specific purpose, such as access for maintenance or a utility line. Understanding the nature and extent of easements on a property is essential for both lenders and borrowers.

For instance, consider a commercial property in West USA Realty with a proposed DSCR loan. If the property has an easement for a utility line that serves a neighboring business, the impact on the property’s cash flow and operations should be meticulously analyzed. The easement may impose certain restrictions on the property owner, such as limited access or specific maintenance obligations, which can affect the overall profitability and stability of the asset. Lenders should assess whether these easements are temporary or permanent, and their potential impact on the property’s value and future revenue streams.

The calculation of easement as part of the financial analysis involves a detailed review of the easement agreement, property records, and relevant market data. Key factors to consider include the frequency and cost of easement-related expenses, potential disruptions to business operations, and the long-term viability of the property’s income generation. For example, a utility easement that requires annual payments could significantly reduce the property’s net operating income (NOI), thereby impacting the DSCR. Lenders should compare the proposed DSCR with historical data and industry standards to ensure the loan remains a secure investment.

Borrowers, on the other hand, need to be transparent about easements and their implications. Disclosing the existence and terms of easements upfront can help streamline the loan application process and prevent surprises later. It enables lenders to conduct a comprehensive financial analysis, ensuring that the loan-to-value (LTV) ratios and interest coverage ratios remain within acceptable ranges. By taking a proactive approach to easement analysis, both lenders and borrowers can navigate the complexities of commercial real estate financing with greater confidence and accuracy.

Documenting Income & Expenses: A Clear Pathway

Documenting income and expenses is a critical aspect of qualifying for a DSCR (Debt Service Coverage Ratio) loan, ensuring lenders can accurately assess a borrower’s financial health. This process involves a comprehensive review of financial records to establish a clear picture of a borrower’s ability to repay. A key element in this evaluation is demonstrating a stable and sustainable cash flow, which can be achieved through meticulous record-keeping of both income and outgoings.

Lenders will scrutinize various income sources, including employment salaries, business profits, rental income, and investment returns. Each source must be verified, often through tax documents, pay stubs, or financial statements. For self-employed individuals or businesses, providing detailed financial records that outline revenue, expenses, and profit margins is essential. West USA Realty, a leading real estate authority, emphasizes the importance of transparency and accuracy in financial documentation, as it facilitates a smoother loan application process.

Expenses, equally as vital as income, need to be categorized and documented to ensure a comprehensive overview. Fixed costs, such as rent, mortgage payments, insurance, and utility easements, offer stability, while variable expenses like groceries, entertainment, and transportation provide a dynamic view of spending patterns. Lenders will assess the reasonableness of these expenses, especially when compared to similar properties in the same area. For instance, a borrower’s utility easement costs should align with industry standards to pass the scrutiny of lenders.

A strategic approach to documenting income and expenses involves organizing financial records chronologically, ensuring all transactions are accounted for. Utilizing accounting software or maintaining meticulous spreadsheets can simplify this process. Additionally, borrowers should be prepared to provide explanations for any discrepancies or unusual expenses. This transparency builds trust with lenders and increases the likelihood of a successful DSCR loan application.

Lender Considerations & Approval Process

When assessing DSCR Loan Requirements, lenders employ a meticulous process that goes beyond mere numbers. West USA Realty, an authority in the real estate sector, highlights that success lies in understanding the interplay of various factors. Each application is unique, requiring lenders to weigh a multifaceted set of considerations. Key among these is the evaluation of easements, specifically utility easements, which can significantly impact property value and loan eligibility.

Lenders scrutinize easement documents to ensure they are legally sound and adequately protect the underlying infrastructure. For instance, a utility easement granting access for power lines or water pipes adds a layer of complexity. Lenders will assess the scope, duration, and conditions of such easements. A broad easement with no specific limitations might raise red flags, while a narrowly defined one, ensuring minimal disruption to property use, could be more favorable. This delicate balance is crucial as it influences both the property’s market value and the borrower’s ability to repay.

The approval process involves a comprehensive analysis of financial statements, appraisals, and credit histories. Lenders often consult with experts to interpret complex easement agreements. West USA Realty emphasizes that transparency and clarity are vital. Borrowers should proactively provide detailed information about any easements, ensuring all relevant data is accessible. This proactive approach facilitates a smoother underwriting process, increasing the likelihood of a successful loan approval. By thoughtfully addressing easement considerations, borrowers can navigate the DSCR loan requirements with confidence, setting the stage for a solid financial foundation.